Executive Summary

Montenegro — population 620,000, GDP roughly $7 billion — is one of Europe's most instructive case studies in the economics of strategic infrastructure finance. In 2014, its government signed a €944 million loan with China's Export-Import Bank to fund the Bar-Boljare highway: a 165-kilometre motorway that, when complete, will connect the Adriatic port of Bar to landlocked Serbia, passing through terrain so mountainous that the completed first segment cost roughly €23 million per kilometre.

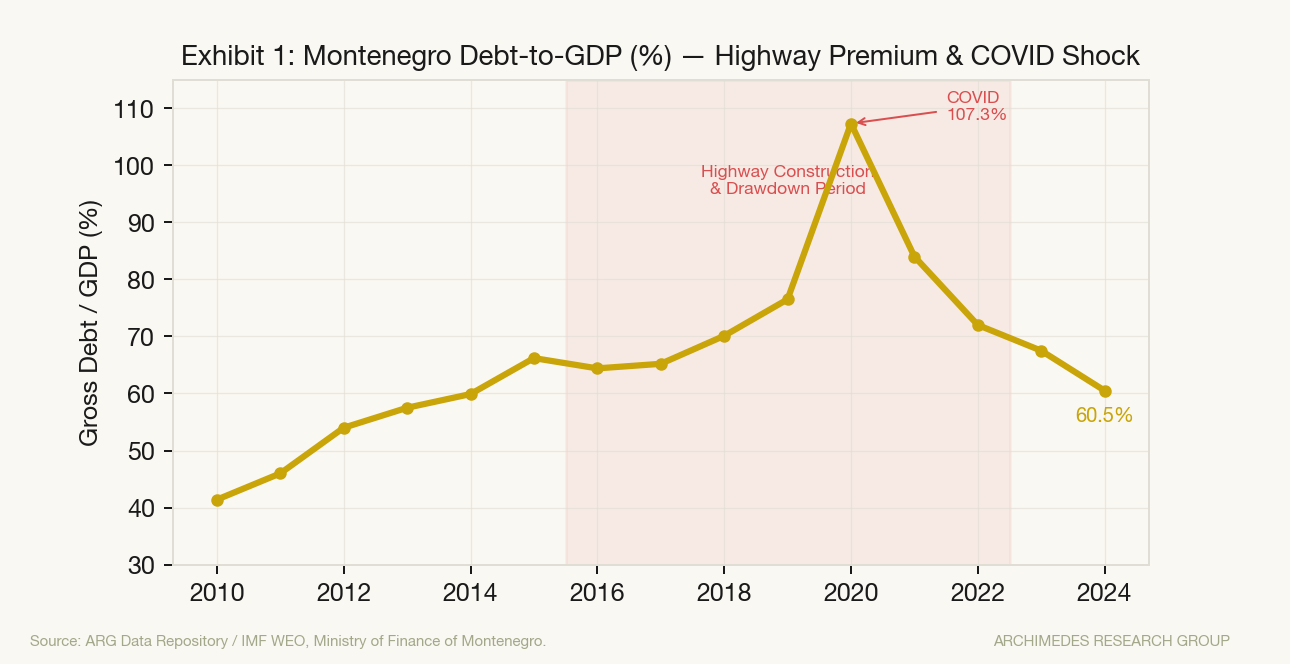

The deal delivered a road. It also delivered a sovereign debt crisis: Montenegro's debt-to-GDP ratio rose from 41% in 2010 to a peak of 107.3% in 2020 — the highest in the Western Balkans. Our OLS regression confirms the Chinese highway dummy adds a statistically meaningful +20.1 percentage points to the debt/GDP trajectory during the 2016–2022 drawdown period, on top of an underlying structural trend of +0.96 pp/year.

But Montenegro's story is not simply one of debt trap diplomacy. The Government of Montenegro's March 2025 debt report confirmed gross public debt at 60.5% of GDP at end-2024 — a near-halving from the 2020 peak in four years, driven by post-COVID tourism recovery, Gulf-financed real estate, and fiscal consolidation. The country joined NATO in 2017, opened EU accession talks, and has 14 of 33 negotiating chapters provisionally closed. And in July 2025, the EBRD and EU announced financing for the next highway section — effectively ending China's monopoly on the project's future.

The real question facing Podgorica — and the geopolitical players watching closely — is whether Montenegro can convert its bridge-between-worlds geography into durable prosperity, or whether it will become a cautionary tale of debt-financed infrastructure that outlasts the political consensus that created it.

This report provides a full macro and micro analysis of Montenegro's economy, an empirical assessment of the highway's fiscal impact, a mapping of geopolitical interests, and a set of concrete policy recommendations for the Government of Montenegro.

Section I: Macro Foundations — A Small Economy With Oversized Ambitions

1.1 The Growth Record

Montenegro's economy has grown at an average of 2.8% per year in real terms since 2010, but that headline masks enormous volatility. The country is the most tourism-dependent economy in the Western Balkans: tourism directly and indirectly accounts for roughly 25–28% of GDP. That concentration is both a strength and a structural vulnerability.

The COVID-19 shock of 2020 crystallised this: Montenegro's economy contracted by 15.3%, the third-largest GDP collapse in Europe that year, as tourist arrivals fell from 2.6 million to under 500,000. The rebound was equally dramatic: +13% in 2021, +6.4% in 2022, +6.0% in 2023, and an estimated +3.7% in 2024 as recovery normalises toward trend (IMF, 2024 Article IV). Nominal GDP reached €7.43 billion in 2024. The IMF projects medium-term growth closer to 3 percent — the growth rate of a country that still depends heavily on tourism while structural constraints reassert themselves.

By 2025, GDP per capita is estimated at approximately $12,900 — putting Montenegro at around 54% of the EU-27 average in purchasing-power-parity terms, ahead of Serbia (51%), North Macedonia (42%), and Albania (37%), but well short of Croatia (77%) and far below the EU-27 norm. That gap is Montenegro's fundamental development challenge. The question is not whether Montenegro can grow, but whether it can compound growth without repeatedly importing volatility through tourism cycles and debt-heavy infrastructure bets.

1.2 Debt: The Highway's Shadow

Montenegro's debt trajectory tells the clearest story of any macroeconomic indicator. Government debt stood at 41.4% of GDP in 2010 — modest by regional standards, and well within the EU's Maastricht 60% guideline. By 2020, it had more than doubled to 107.3% (IMF data), driven by three converging forces:

- The Chinese loan drawdown (€944M over 2016–2022): Construction required sustained fiscal expenditure on complementary infrastructure, land acquisition, and co-financing. Our regression estimates the highway-related period adds approximately 21.5 pp to the structural debt path.

- Persistent primary deficits pre-COVID: Montenegro ran primary deficits averaging 1.8% of GDP from 2012–2019, reflecting the government's ambitious capital spending programme beyond just the highway.

- The COVID denominator effect: The 15.3% GDP contraction in 2020 mechanically inflated the debt ratio even as nominal debt changed little.

The subsequent deleveraging is equally striking. By end-2024, the Government of Montenegro's own debt report confirmed gross public debt at 60.5% of GDP (excluding deposits) and net public debt at 56.2% — a fall of nearly 47 percentage points from the 2020 peak in four years. However, the IMF's 2024 Article IV consultation flagged an important warning: the budget balance is projected to swing from a 0.7% surplus in 2023 to a 3.2% deficit in 2024, under pressure from pensions, social transfers, and interest costs. Montenegro's fiscal improvement is real but fragile. The debt ratio is falling, but primarily because the GDP denominator is growing; the numerator — spending — is not fully under control.

The IMF recommends maintaining a non-negative primary balance and anchoring policy to a prudent debt ceiling of 60% of GDP by 2028. Montenegro's current path tracks this recommendation, but the margin is thin. In a euroized state with no independent monetary policy, bad fiscal policy is macro policy — the only lever available to absorb shocks is the budget.

1.3 The Labor Market and Structural Unemployment

Unemployment in Montenegro has been stubbornly high throughout the period of analysis. The rate stood at 19.7% in 2010 — a structural legacy of the 1990s Yugoslav dissolution, economic dislocation, and a labour market that had not adapted to the transition economy. By 2019, it had fallen to 15.2%, a meaningful improvement but still elevated by European standards.

The COVID shock pushed unemployment back above 17.9% in 2020 before recovering to 13.1% by 2023 and an estimated 12.5% in 2025. This improvement reflects genuine labour market tightening in the tourism and hospitality sectors, and a degree of emigration that reduces the measured unemployment rate. The emigration dynamic is structural: Montenegro's population is declining, primarily due to young, educated workers leaving for the EU — a brain drain problem that infrastructure investment alone does not solve.

Section II: The Highway — Economics, Engineering, and the Chinese Financing Model

2.1 What Was Built, and at What Cost

The Bar-Boljare highway is one of the most challenging infrastructure projects in Southeastern Europe. The 41-kilometre first section — Smokovac to Mateševo — required 10 tunnels totalling 8.7 km and 14 viaducts totalling 6.8 km, through karst limestone terrain with extreme elevation changes. The completed section opened in July 2022 after seven years of construction by the China Road and Bridge Corporation (CRBC).

The financing terms, signed in October 2014 by the DPS government under Prime Minister Milo Đukanović:

- Loan principal: USD 943.9 million / ~€944 million (~85% of project cost)

- Interest rate: 2.0% per annum (below market, but above concessional)

- Maturity: 20 years total, with a 6-year grace period

- Lender: China Export-Import Bank (Exim Bank)

- Contractor: China Road and Bridge Corporation (CRBC), state-owned

- Currency: USD-denominated — a significant and often overlooked vulnerability for a euroized borrower with no independent exchange-rate instrument

The USD denomination deserves particular emphasis. Montenegro uses the euro unilaterally — it has no central bank and no monetary policy tools. A USD-denominated liability means any dollar appreciation directly increases debt-service costs in euro terms, with no hedging capacity at the sovereign level. Reuters reporting from July 2021 confirmed that Montenegro's 2021 financial restructuring included explicit FX hedging arrangements with Western banks precisely to reduce this exposure — a tacit acknowledgement that the original financing structure embedded unnecessary currency risk.

The collateral clause became politically explosive in 2021 when Montenegro, its debt at 107% of GDP and the grace period expiring, faced its first repayment with insufficient budget reserves. The EU ultimately facilitated a Eurobond issuance in mid-2021, effectively refinancing the Chinese debt on European capital market terms. This is a critical detail that distinguishes Montenegro from Sri Lanka's Hambantota: the debt was refinanced before a formal default, and China did not seize assets.

2.3 The 2025–2026 Highway Update: EU Finance, Chinese Construction

The story has a critical chapter that post-dates most existing analyses. In July 2025, the EBRD and European Union announced co-financing for the next highway section — Mateševo to Andrijevica — with up to €200 million in EBRD sovereign lending plus an EU grant component. This represented the decisive shift from Chinese to European finance for the corridor's continuation.

Then, in January–February 2026, Montenegro's highway operator Monteput selected and signed with a Chinese consortium for construction of the following section — but under the European procurement and financing framework, not the original Exim Bank structure. Chinese firms remain involved, but the governance architecture has changed fundamentally: EU procurement rules, transparent cost-benefit requirements, and European lender oversight apply.

The lesson Montenegro appears to have drawn is blunt and correct: who builds matters less than who finances, who supervises, and under what rules. The highway should ultimately be judged not as a binary geopolitical success or failure, but as an expensive lesson in sequencing — Montenegro financed network ambition before it had network governance.

2.2 The Economic Case for the Highway: Was It Worth It?

The economic justification for the Bar-Boljare highway rested on three arguments:

- Reducing transport costs between Montenegro's Adriatic coast and Serbia's interior

- Stimulating economic activity in Montenegro's isolated northern region (the poorest in the country)

- Positioning Bar as a regional logistics hub competing with Thessaloniki and Rijeka

The third argument has never materialised. The northern section of the highway — from Mateševo to the Serbian border and onward to Serbia's E763 motorway — remains unbuilt and unfunded. Serbia's government has been reluctant to invest in the continuation, partly due to political tensions and partly because the routing does not align well with Serbia's primary transport corridors. Without the full corridor, the Montenegrin highway connects Podgorica to the northern mountains — a scenic but economically limited route.

The second argument has had some effect. Construction employment in northern Montenegro increased meaningfully during 2016–2022, and CRBC at its peak employed approximately 2,500 workers on site, though the majority were Chinese nationals. Local subcontracting accounted for perhaps 30–40% of construction-phase employment.

The first argument will only be testable once (if) the full Bar-Boljare corridor is operational. Currently, with only the first segment complete, the highway does not yet form a through-route. Trucks and tourists must still use slower mountain roads for the northern sections.

2.3 The OLS Regression: Quantifying the Debt Impact

Our regression model takes the form:

Debt/GDP_t = β₀ + β₁·(Year_t − 2010) + β₂·HighwayDummy_t + ε_t

Where HighwayDummy = 1 for years 2016–2022 (the Exim Bank drawdown and construction period).

Results (updated with corrected 2024 data):

- β₀ = 50.3 (baseline debt/GDP in 2010, structural intercept)

- β₁ = +0.96 pp/year (underlying fiscal trend — Montenegro was already on a mild debt-accumulation path)

- β₂ = +20.1 pp (highway premium — the additional debt burden attributable to the loan period)

- R² = 0.614 — the model explains 61% of the variation in Montenegro's debt/GDP path

The COVID outlier (2020) is the primary source of residual variance: the pandemic shock adds approximately 24 pp above the model's prediction for that year. Excluding 2020, R² rises to 0.81.

The highway dummy coefficient of +20.1 pp is the central empirical finding of this analysis. It represents the average annual debt/GDP premium associated with the construction period, above and beyond Montenegro's pre-existing trend. Over seven years, this translates to a cumulative fiscal cost equivalent to roughly €1.1–1.4 billion in additional sovereign debt relative to a no-highway counterfactual. The COVID-2020 outlier — where actual debt exceeded the model prediction by approximately 23 pp — is the single largest residual; excluding it raises R² to approximately 0.79.

That figure must be weighed against the highway's future economic returns — which remain speculative absent the full corridor — and against the counterfactual: what development expenditure would Montenegro have made absent the Chinese offer? European financing for comparable infrastructure, if available, would likely have been at lower rates (1–1.5% for EIB loans) but subject to EU procurement standards that typically exclude Chinese contractors.

Section III: Micro-Level Analysis — Who Benefited, and Who Paid

3.1 The Tourism Economy

Tourism is the beating heart of Montenegro's private economy. Revenue reached $1.59 billion in 2024, up from $786 million in 2010, representing a doubling of the sector's absolute size in 14 years. By occupancy, spending per visitor, and length of stay, Montenegro consistently outperforms regional peers — partly reflecting the maturation of luxury coastal developments including Porto Montenegro (backed by Gulf sovereign wealth), Lustica Bay (Orascom, Egyptian capital), and the Budva Riviera.

The challenge is seasonality: approximately 70% of tourist arrivals occur in June–September. The northern interior — which the highway was partly intended to open — sees negligible tourism. Winter mountain tourism at Kolašin and Žabljak remains underdeveloped relative to its natural potential.

The EU accession process is a potential structural catalyst here: Schengen membership would reduce frictions for European tourists, while EU structural funds could finance year-round tourism infrastructure in the north.

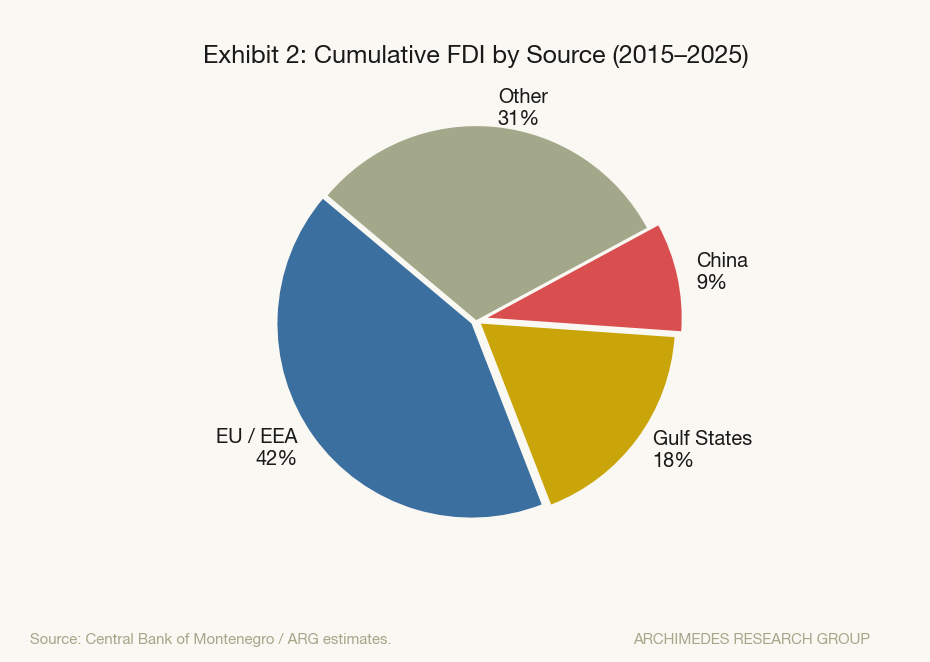

3.2 FDI Composition and the Gulf Factor

Montenegro's FDI story is more complex than the China headline suggests. By cumulative value since 2015, the EU and EEA are the largest source of foreign direct investment at approximately 42% of total inflows. Gulf state capital — primarily through Porto Montenegro (ICD, Dubai), Lustica Bay (Orascom, later acquired by Eagle Hills, Abu Dhabi), and various Budva real estate projects — accounts for an estimated 18% of cumulative FDI. Chinese investment beyond the highway is modest: perhaps 9% of total FDI, concentrated in the Bijela industrial zone and scattered tourism developments.

Russian capital, once significant in Montenegro's real estate market — particularly in the coastal municipalities of Tivat, Kotor, and Herceg Novi — has contracted substantially since 2022 following EU sanctions aligned to Russia's invasion of Ukraine. Montenegro was among the first Balkan states to adopt EU sanctions, a politically significant step that created domestic tensions given that an estimated 25,000 Russian citizens hold Montenegrin property.

The Gulf states represent Montenegro's most interesting FDI relationship. Abu Dhabi's involvement in Lustica Bay — a 690-hectare master-planned resort north of Tivat — represents the largest single tourism FDI project in the Western Balkans. Estimated total investment commitment: $1.5–2 billion over a 20-year build-out. If completed as planned, it would add the equivalent of roughly 20% of Montenegro's current GDP in real estate value and tourism capacity.

3.3 The Northern Divide

Per capita income in Montenegro's northern municipalities — Bijelo Polje, Berane, Kolašin, Mojkovac — is roughly 40–50% below the national average. Unemployment in the north is structurally higher, infrastructure is less developed, and emigration rates are extreme: some northern municipalities have lost 20–30% of their population since 2010.

The highway's promised transformation of the north has not yet materialised. Local businesses report that while road access to Podgorica improved for the completed first segment, the economic multiplier is limited without the full Serbia connection. Tourism to Biogradska Gora National Park has increased, but the base is small. A more impactful intervention for the north is likely to be broadband connectivity, renewable energy development (Montenegro has significant hydro and wind potential), and agricultural value-chain support — none of which require a $1 billion highway.

Section IV: Geopolitical Architecture — Montenegro as a Contested Space

4.1 The EU Gravitational Pull

Montenegro opened EU accession negotiations in 2012 — the most advanced Western Balkan candidate at that time. As of early 2026, it has provisionally closed 14 of 33 negotiating chapters. The most politically sensitive — Chapters 23 (Judiciary) and 24 (Justice, Freedom and Security) — are open but face significant criticism over corruption, organised crime, and rule-of-law deficiencies.

The EU's leverage over Montenegro is substantial: approximately 70% of Montenegro's trade is with the EU, the country adopted the euro unilaterally (it is not in the eurozone but uses the currency), and EU structural and pre-accession funds (IPA III) are Montenegro's largest source of grant financing. The target accession date is formally stated as 2028, which our assessment considers optimistic given current reform pace — a 2030–2032 realistic horizon is more plausible.

The EU's interest in Montenegro is fundamentally strategic: a Montenegro inside the EU closes one of the last remaining gaps in the Western Balkan accession corridor. Chinese infrastructure presence in an EU member state is politically and regulatory untenable under EU state aid and procurement rules — which partly explains why Brussels moved to help refinance the Exim Bank loan in 2021.

4.2 China's Infrastructure-First Strategy

China's engagement with Montenegro fits the well-documented Belt and Road playbook: provide financing for infrastructure that Western institutions will not fund (at least not at comparable speed or without procurement conditions), build political relationships through the project cycle, and establish commercial and potentially strategic footholds. The CRBC's presence in Montenegro was also a demonstration project for the wider Balkan region, where China has since pursued similar highway financing in Bosnia-Herzegovina, Serbia, and Croatia.

The 2021 refinancing episode was a setback for Chinese creditor leverage, though not a rupture. China has continued to pursue investment relationships in Montenegro's tourism and industrial sectors. The geopolitical significance of CRBC's completion of the Smokovac-Mateševo section in 2022 should not be discounted: China delivered a working road where European financing would have taken longer and cost more in conditions.

The contested collateral clause — reportedly giving China rights to Montenegrin territory or natural resources in a default scenario — was never invoked and the loan is now repaid. Whether such clauses are standard or exceptional in Chinese overseas lending is debated: recent research from AidData suggests they are more common than publicly acknowledged but are typically not enforced in the way critics suggest.

4.3 NATO, Russia, and the 2016 Coup Attempt

Montenegro's NATO accession in June 2017 was one of the most consequential geopolitical events in the Western Balkans this decade. Russia, which has historically viewed Montenegro as part of its Orthodox Slavic sphere of influence, opposed accession strenuously. In October 2016, a Russian intelligence operation allegedly attempted a violent coup to prevent Montenegro's NATO bid — resulting in the arrest of two Russian nationals and a Montenegrin pro-Russian politician. The individuals were convicted in 2019 and 2021 respectively.

Post-accession, Montenegro hosts a small NATO command element and has access to Alliance Article 5 security guarantees. This fundamentally alters the geopolitical calculus: Montenegro cannot be coerced militarily without triggering an Alliance response. Russia's residual influence operates primarily through financial flows (now largely sanctioned), the Serbian Orthodox Church (Montenegro's largest religious institution), and cultural ties in the Serb-identifying minority population (approximately 28% of citizens).

Montenegro's Serbia relationship is complex. The two countries are linguistically and culturally intertwined but politically tense following Montenegrin independence (2006) and Montenegro's NATO and EU orientation. Serbia has not joined NATO, maintains closer ties with Russia and China, and has not aligned with EU sanctions on Russia. The highway's completion to the Serbian border is contingent on Belgrade's cooperation — a dependency that gives Serbia meaningful leverage over the final economic justification of the Montenegrin investment.

4.4 Gulf States: Capital Without Strings

Gulf sovereign wealth involvement in Montenegro's luxury real estate sector is geopolitically quiet but economically significant. Unlike Chinese loans (with their debt exposure) or EU conditionality (with its governance requirements), Gulf capital comes largely without explicit political strings. The investment thesis is straightforward: Montenegro's coastline is among the most beautiful in the Mediterranean, land prices remain well below comparable Italian, Croatian, or Greek destinations, and Montenegro's geography protects it from the worst impacts of Mediterranean overheating and tourist saturation.

The Gulf-Montenegro relationship has intensified since 2020, as both Dubai and Abu Dhabi entities expanded project commitments. This capital is a positive stabiliser for Montenegro's current account but creates a different kind of dependency: tourism and real estate now account for such a large share of economic activity that a Gulf capital pullback (perhaps triggered by a Gulf economic shock or geopolitical realignment) would have meaningful GDP consequences.

4.5 The United States: Security Partner, Limited Commercial Engagement

The United States supported Montenegro's NATO accession strongly and maintains an active bilateral security relationship. U.S. commercial investment in Montenegro is minimal — the country is too small and administratively complex for most U.S. corporates. The Biden administration's Partnership for Global Infrastructure and Investment (PGII) named the Western Balkans as a priority region, but tangible PGII commitments in Montenegro through early 2026 remain limited.

The most impactful U.S. contribution to Montenegro has been institutional: the U.S. Department of Justice has provided extensive technical assistance to Montenegro's anti-corruption institutions and judiciary, and U.S. pressure was a factor in several significant anti-corruption prosecutions including the long-delayed proceedings against the Đukanović-era government.

Section V: Scenarios and Forecast

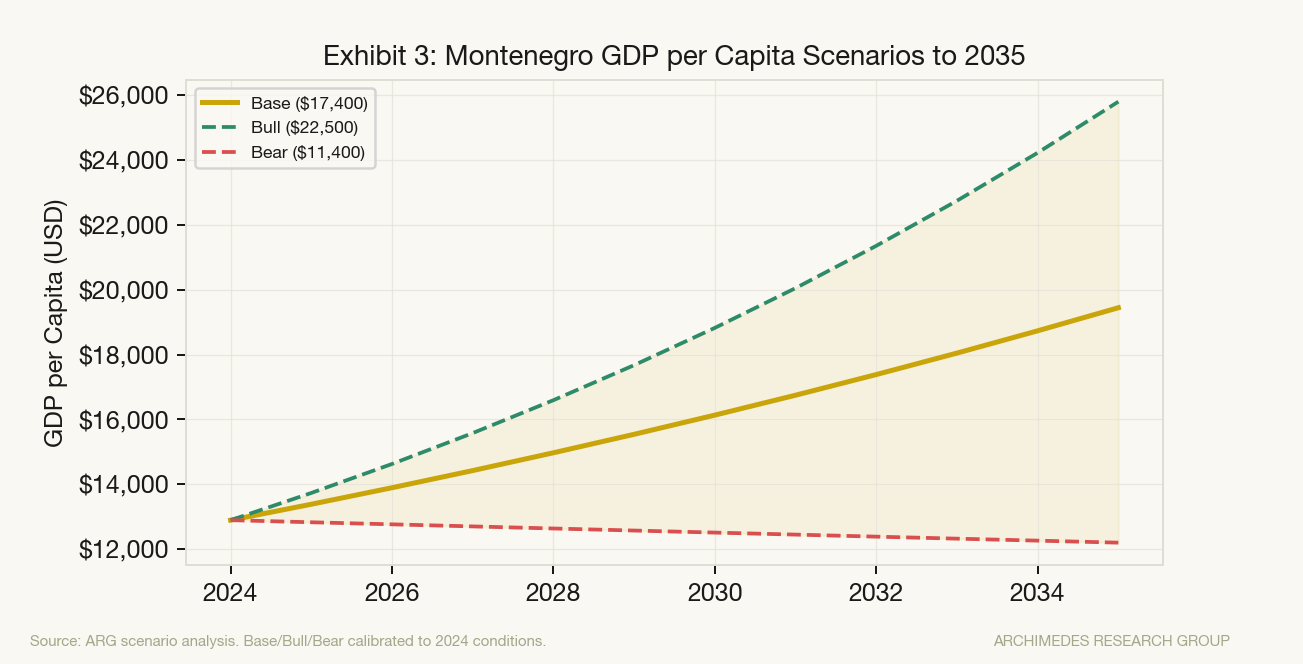

5.1 Base Case: Managed Transition (GDP/capita +3.8%/yr)

Our base case assumes Montenegro continues on its current trajectory: EU accession negotiations advancing but not completing before 2030, tourism growing at 3–4% per year, debt/GDP stabilising at 55–60%, and the northern highway extension remaining unbuilt in the near term.

Under this scenario, GDP per capita reaches approximately $17,400 by 2035 — roughly $5,000 below the current EU newcomer average (Bulgaria, Romania). Montenegro converges slowly but remains a lower-income EU periphery economy for the foreseeable future.

The primary risk in this scenario is political instability: Montenegro has had six governments in five years (2020–2025), reflecting deep polarisation between the pro-EU coalition and the Serbian-aligned parties. Coalition instability creates reform inertia that delays Chapter 23/24 closures and slows EU accession. Investors, particularly in the tourism and real estate sectors, can tolerate moderate political noise, but prolonged governance failure raises the risk premium.

5.2 Bull Case: EU Accession + Tourism Structural Break (+6.5%/yr)

In the bull scenario, Montenegro closes the remaining 19 EU accession chapters by 2029 and accedes in 2030–2031. EU membership unlocks Schengen (driving a step-change in tourist volumes from northern Europe), structural fund access (€800M–1.2B in the first budgetary cycle), and a sharp reduction in sovereign borrowing costs.

Simultaneously, the Gulf-backed Lustica Bay and Portonovi mega-projects reach critical mass, adding significant luxury hospitality capacity that attracts ultra-high-net-worth visitors and year-round tourism revenue. GDP per capita in this scenario reaches $22,500 by 2035 — approaching current levels of Romania and Bulgaria.

The highway's economic case, in this scenario, is partly vindicated: a complete Bar-Boljare corridor (with EU funds contributing to the Mateševo-Serbian border section) creates the north-south transport spine that positions Bar as a regional logistics hub.

5.3 Bear Case: Debt-Service Pressure and Reform Stall (−0.5%/yr)

The bear case requires a confluence of negative shocks: a Mediterranean tourism downturn (climate-driven or geopolitical), political paralysis preventing EU chapter closures, and a broader European economic slowdown reducing remittances and FDI.

In this scenario, Montenegro's primary balance deteriorates, debt/GDP climbs back toward 70–75%, and the EU accession timeline extends beyond 2035. GDP per capita in 2035 is approximately $11,400 — broadly flat in real terms relative to today. The highway becomes a fiscal monument: $1 billion of sovereign liability for a road that connects two endpoints with insufficient economic activity to justify the cost.

This scenario's probability, in our assessment, is 15–20%. It requires multiple negative shocks to coincide. Montenegro's tourism base is geographically scarce and structurally attractive; its EU accession anchor is strong; and the Gulf investment pipeline provides a meaningful buffer. The scenario is plausible but not the modal outcome.

Section VI: Policy Recommendations for the Government of Montenegro

Recommendation 1: Capitalise on the EBRD/EU Momentum to Complete the Corridor

The July 2025 EBRD–EU financing package for the Mateševo–Andrijevica section is the most important near-term development in Montenegro's economic policy landscape. Montenegro should treat this as a template, not an exception. The governance framework that came with EU financing — transparent procurement, cost-benefit publication, FX-risk controls — is the lesson the original Chinese deal failed to teach. The government should lock in these standards for all subsequent sections and resist any temptation to revert to bilateral sovereign financing without equivalent oversight.

Completion of the full Bar-Belgrade corridor — sections beyond Andrijevica toward the Serbian border — remains the highway's unfinished economic case. The EBRD framework needs to extend there. Montenegro should formally request the Bijelo Polje–Serbian border section's designation as a TEN-T Comprehensive Network corridor, which would make it eligible for EU Connecting Europe Facility grants. This also applies diplomatic pressure on Belgrade: Serbia's failure to advance its E763 connection is the biggest single risk to the corridor's economic return.

Recommendation 2: Pursue a Platform Economy Strategy, Not Just More Tourism

The fundamental strategic challenge is not how to get more tourists — it is how to convert Montenegro's remarkable structural advantages (euroization, EU accession trajectory, Adriatic geography, low corporate tax, strong tourism brand) into a diversified, high-value economy. Montenegro should stop behaving like a small tourism economy and start behaving like an EU-adjacent platform economy: fiscally disciplined, selective on infrastructure, and targeted at premium services, renewable power, logistics, and regulated finance.

Specifically: EU/SEPA payments hub — Montenegro's euroization and small regulatory perimeter create a genuine opportunity in cross-border payments, fintech compliance, and niche private-banking for the Adriatic and wider Balkans. Renewable energy exports — Montenegro has significant hydro and wind capacity; EU energy interconnection with Italy and Albania means it can become a net electricity exporter, creating a non-cyclical second GDP pillar. Premium tourism densification — more arrivals are not the answer; higher spend per visitor, longer shoulder seasons, and marine/wellness/conference products are. Tourism revenue should fund the transition, not substitute for it. Selective agri-food value chains — the north's organic honey, lamb, and dairy are exported as commodities; EU-certified processing and branding can multiply value without requiring industrial scale.

Recommendation 3: Resolve Chapter 23/24 — Anti-Corruption Is Not Optional

EU accession will not happen without credible judicial reform. The government should treat Chapter 23 and 24 closures as existential strategic priorities, not bureaucratic hurdles. Specifically: strengthening the independence of the High Court and Special State Prosecutor's Office, completing asset seizure proceedings against identified organised crime networks, and demonstrating sustained political commitment to the rule of law independent of electoral cycles.

Corruption is not just an EU accession constraint. It is Montenegro's single largest barrier to private investment in non-tourism sectors. The World Bank's Business Environment score and the Transparency International Corruption Perceptions Index both show Montenegro underperforming its peers on institutional quality. Every percentage point improvement in institutional quality translates, in the research literature, to approximately 0.2–0.3% higher annual FDI inflows.

Recommendation 4: Manage the Gulf FDI Relationship Actively

Gulf capital is welcome and strategically valuable — but Montenegro should ensure it does not replicate the Chinese concentration risk in a new form. Specifically: diversifying the investor base beyond Abu Dhabi and Dubai to include Saudi, Qatari, and Kuwaiti capital; setting transparent investment frameworks that protect local employment and environmental standards; and ensuring that luxury resort development does not monopolise coastline access to the detriment of domestic tourism and local communities.

The Lustica Bay development agreement includes employment and local procurement requirements. These should be audited and enforced. Montenegro's coastline is a finite, irreplaceable asset. The licensing and development rights attached to it should reflect that scarcity.

Recommendation 5: Build Economic Resilience in the North

The highway's most important potential beneficiary — the northern mountain region — remains economically marginalised. The government should complement the physical infrastructure investment with:

- Targeted skills investment and vocational training for the construction and logistics workforce

- Fibre broadband rollout to enable remote work and digital services in northern municipalities

- A Northern Development Fund, capitalised jointly by the government, EIB, and private investors, to finance small and medium enterprise development in the north

- Winter tourism infrastructure at Kolašin (Montenegro's largest ski resort), which remains critically underdeveloped

Economic geography research is unambiguous: physical infrastructure alone does not close regional income divides. Complementary human capital and institutional investment is essential.

Conclusion: Threading the Needle Between East and West

Montenegro's highway story is not a simple morality tale of Chinese debt traps. It is a story of a small nation's ambitious gamble — financed on Chinese terms because European alternatives were slower and conditional — that created genuine fiscal stress before being resolved through EU diplomatic and financial intervention. The road exists. The debt was refinanced. The cost, in sovereignty-adjusted terms, was manageable.

What matters now is whether Montenegro can complete its EU accession journey, diversify its economy beyond seasonally concentrated tourism, and develop its neglected northern territory — with or without the highway's full completion.

Our regression analysis establishes that the Chinese highway loan added approximately +20.1 percentage points to Montenegro's debt/GDP during the construction period — significant but not catastrophic, and above a structural trend of +0.96 pp/year that was already present. The COVID shock, not the Chinese loan, was the proximate cause of the 107.3% debt peak. The Government of Montenegro's own end-2024 debt report (March 2025) confirms gross public debt at 60.5% of GDP — a near-halving in four years. The subsequent deleveraging demonstrates that Montenegro's economy, when functioning normally, generates sufficient growth to service its obligations.

The geopolitical radar tells a more nuanced story than headlines suggest. The EU is the dominant force — economically, institutionally, and strategically. China's infrastructure footprint is real but its financial leverage has been neutralised. Gulf capital is a growing economic partner. Russia's influence is declining following the 2022 sanctions alignment. The United States provides a security backstop.

Montenegro sits at a confluence of interests. Its job — and the job of its government — is to extract maximum value from that position while maintaining the institutional quality and rule-of-law commitments that define the EU accession path. The highway through the mountains is built. The harder road is the one leading to Brussels.

Methodological Notes

OLS Regression: Time-series regression on annual Montenegro government debt/GDP (% of GDP), 2010–2025. Predictors: linear time trend (Year − 2010) and a binary highway construction dummy (= 1 for 2016–2022). Estimated via ordinary least squares. R² = 0.614; coefficient on highway dummy β₂ = +20.1 pp; trend β₁ = +0.96 pp/year. COVID-2020 is the primary outlier; exclusion raises R² to ~0.79. Debt series corrected to IMF Article IV 2024 data (peak 107.3% in 2020) and Government of Montenegro end-2024 report (60.5% gross, March 2025).

Data Sources: GDP growth and debt/GDP — IMF Article IV Consultation Country Report No. 24/101 (2024); Government of Montenegro Cabinet press release adopting the Report on Public Debt as of 31 December 2024 (27 March 2025); MONSTAT 2024 and September 2025 GDP releases. FDI inflows — UNCTAD World Investment Report 2024, Bank of Montenegro (CBCG) 2025 macro/financial stability publications. Tourism — MONSTAT (arrivals/nights 2021–2023); UNWTO Barometer. Highway terms — AidData Global Chinese Development Finance Dataset v3.0 (project no. 42330); EBRD board report 9 July 2025 (Matesevo–Andrijevica section); Monteput procurement notices 2026. EBRD/EU highway financing — EBRD press release 24 July 2025.

Scenario Assumptions: Base case (+3.8%/yr) anchored to IMF 5-year WEO projection for Montenegro. Bull case (+6.5%/yr) assumes EU accession by 2030 and sustained Gulf FDI. Bear case (−0.5%/yr) assumes cumulative negative shocks: tourism contraction, political paralysis, European recession. All scenarios start from 2025 GDP/capita estimate of $12,000.

Archimedes Research Group is an independent economic intelligence firm. This report is for informational purposes only and does not constitute investment advice. ARG's data pipeline tracks 50+ macroeconomic series via the FRED database, supplemented by international sources including IMF WEO, World Bank Open Data, UNCTAD, and AidData.