The Paradox

On the surface, the February 2026 Job Openings and Labor Turnover Survey (JOLTS) looks like a mixed bag: 6.9 million open positions still dot the ledger, unemployment sits at 4.4 percent, and there is no mass-layoff event to headline. But one data point cuts through the noise. The hiring rate — new hires as a share of total employment — fell to 3.1 percent in February, the lowest reading since April 2020, when large swaths of the American economy were physically shuttered. Outside of that extraordinary period, it is the weakest hiring pace since 2011.

That number demands more than a passing mention. The economy is open. Companies are posting jobs. Workers are showing up to apply. Yet the rate at which employers are actually converting openings into new employees has collapsed to pandemic-era depths. What we are witnessing is not a recession in the conventional sense — it is something more insidious: a labor market frozen in place.

The Phantom Openings Paradox

The headline figure of 6.9 million job openings can create a misleading sense of dynamism. Openings are a stock, not a flow; they tell us how many positions employers say they want to fill, not how aggressively they are pursuing that goal. The flow metric — actual hires — tells a very different story. Hires fell to 4.849 million in February, roughly 498,000 fewer than January and the lowest monthly count since the onset of the pandemic. The ratio of openings to hires, normally a measure of labor market tightness, has morphed into a measure of employer ambivalence.

This divergence is sometimes called the "phantom opening" problem: job postings that exist on company career pages but are not actively being filled, maintained as signals of growth intent rather than genuine near-term demand. In a period of acute policy uncertainty, keeping a requisition open costs little and preserves optionality, while adding headcount locks in fixed costs for months or years. Rational corporate behavior in an irrational policy environment.

Workers Who Won't Quit

Equally telling is the quits rate, which measures voluntary separations as a share of employment — a proxy for worker confidence in the labor market. In February it registered 1.9 percent, the eighth consecutive month at or below the 2.0 percent threshold. That eight-month streak has no peacetime precedent in the post-2001 JOLTS history. Workers are not quitting, not because they love their current jobs, but because they don't trust the market on the other side of the door.

A labor market where neither side is moving — employers won't hire, workers won't quit — is not stable equilibrium. It is a compressed spring.

The calculus is asymmetric and reinforcing. Employers who see weak hiring across the economy become more reluctant to expand themselves. Workers who see a hiring rate at COVID lows become more reluctant to leave the job security they have. The result is a self-sustaining stasis that can persist — until it cannot.

The Tariff Transmission Mechanism

The proximate cause of this paralysis is traceable to policy, specifically the prolonged uncertainty surrounding U.S. trade and tariff strategy. Following the Supreme Court's February 2026 ruling that broad IEEPA-based tariffs are unconstitutional, the Administration shifted to Section 122 authorities, imposing a fresh round of tariffs of up to 15 percent on all imports for a 150-day period. The legal and commercial landscape for companies with global supply chains has been in near-constant flux for the better part of fourteen months.

Our internal tariff uncertainty index, constructed from news flow and sentiment data, averaged 47 points in January and February before declining to 18 in March — reflecting the brief respite that followed the court ruling and the Section 122 replacement regime. But the damage to hiring confidence was already done. Businesses do not pause hiring one month and resume the next as soon as a legal ruling clarifies a tariff statute. Planning cycles, budget approvals, and headcount authorizations operate on quarters, not weeks.

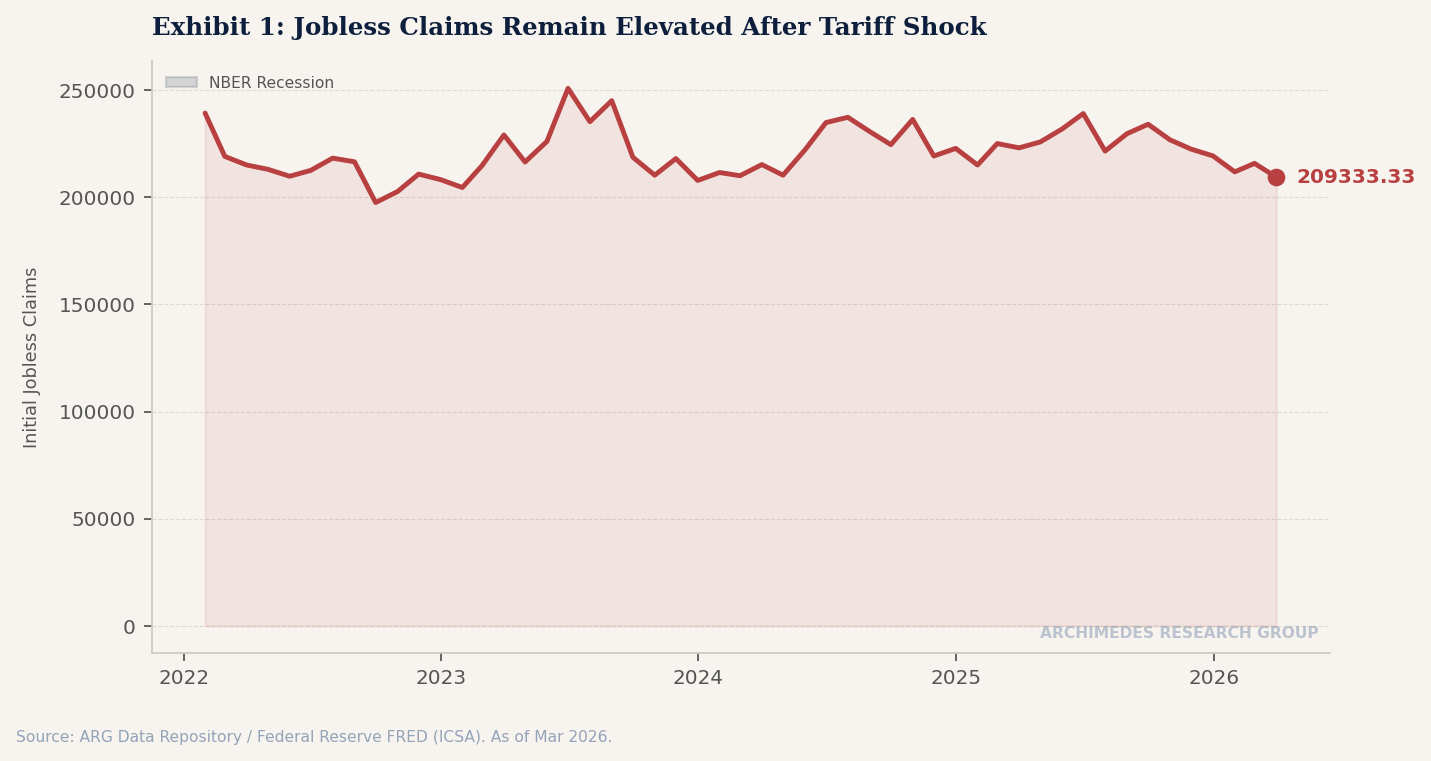

The macro confirmation is visible in our broader data. Consumer sentiment (UMCSENT) has ranged between 51 and 61 for most of the past twelve months — below the long-run median but not signaling acute distress. Initial jobless claims (ICSA) remain contained near 215,000, suggesting layoffs have not yet accelerated. The Chicago Fed National Financial Conditions Index (NFCI) sits at approximately −0.54, indicating conditions that remain modestly accommodative. These are not the readings of an economy in free fall. They are the readings of an economy that has stopped moving forward.

What the ARG Recession Model Says

The Archimedes Research Group recession probability model — a probit framework built on yield curve spreads, financial conditions, initial claims, payroll growth, and unemployment dynamics — currently estimates a 13.1 percent probability of a recession within the next twelve months, as of the February 2026 data vintage. That is well below the 40-plus percent readings the model generated in the spring of 2025, and sits in a range that would historically be classified as "elevated but non-recessionary."

Importantly, the yield curve has re-steepened meaningfully. The 10-year/3-month spread (T10Y3M) moved from deeply negative levels in early 2024 to approximately +0.44 in February 2026, removing one of the model's most powerful recessionary signals. The Federal Reserve's posture has also shifted toward accommodation at the margin. In isolation, these financial-conditions variables argue against imminent recession.

The tension — and the risk — lies precisely in this gap between what financial markets are pricing and what the labor flow data is showing. Financial conditions indicators reflect asset prices and credit spreads, which can remain benign while the real economy quietly decelerates. JOLTS is a real-economy measure. A 3.1 percent hiring rate with a 1.9 percent quits rate is the labor market's way of filing a dissenting opinion against the consensus narrative of contained risk.

What to Watch in the Coming Months

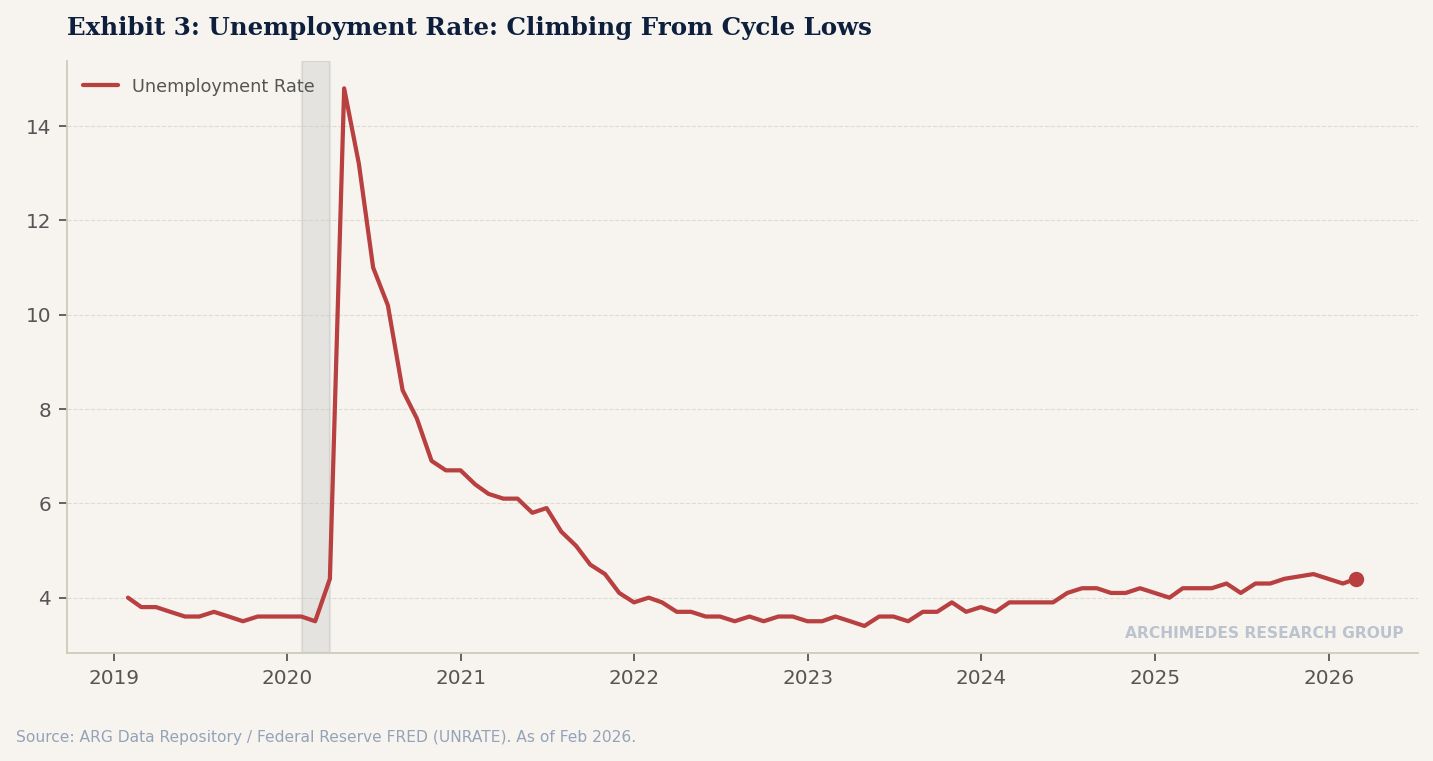

The March jobs report, due this week, will be the first critical test of whether February's JOLTS deterioration was a transient disruption or the beginning of a trend. If nonfarm payrolls disappoint and the unemployment rate edges above 4.5 percent, the Sahm Rule — which flags recession when the 3-month moving average of unemployment rises 0.5 percentage points above the prior year's low — will draw renewed attention. We are not there yet, but the buffer has narrowed.

Beyond the headline numbers, we will be watching JOLTS hires closely. A second consecutive month below 4.9 million would confirm the February reading was not noise. We will also be monitoring the gap between job openings and actual hiring: if openings begin to fall materially, it would suggest that phantom postings are being withdrawn — a more concrete signal that employers are resetting expectations downward, not merely deferring decisions.

Finally, policy resolution matters more than almost any data point. The 150-day Section 122 tariff clock runs through mid-summer. If trade negotiations yield meaningful agreements — as has already occurred with more than twenty trading partners — corporate confidence could recover faster than the labor data alone would suggest. The frozen spring can thaw quickly when the policy temperature rises.

For now, the February JOLTS report is a warning filed in careful language. The hiring machine has not broken down. It has simply stopped. That distinction matters — until it doesn't.

Disclaimer: This article is published for informational and research purposes only and does not constitute investment advice. The ARG recession probability model is a quantitative tool based on historical patterns; it should not be interpreted as a forecast of any specific economic outcome. All data sourced from the U.S. Bureau of Labor Statistics, Federal Reserve Economic Data (FRED), and Archimedes Research Group internal models. Past model performance does not guarantee future accuracy.