Executive Takeaway

The February 2026 JOLTS release shows the U.S. labor market is no longer simply "normalizing" — it is bifurcating. Job openings have fallen to roughly 7.2 million, the lowest print since early 2021, while the quits rate has slipped to 1.9%, a level historically associated with stalling nominal wage growth rather than soft-landing equilibrium. Payrolls remain superficially firm, but the flows — hires, quits, and openings per unemployed — are deteriorating in a pattern more consistent with a late-cycle inflection than mid-cycle cooling. For the Fed, this strengthens the case for a Q3 cut; for credit and consumer-exposed equities, it raises the probability of a second-half earnings downgrade cycle that consensus is not yet reflecting.

What the Data Actually Says

Three shifts stand out in the latest JOLTS print. First, the vacancy-to-unemployed ratio has compressed to roughly 1.02, down from a peak above 2.0 in 2022 and now below the 2018–2019 average — the Fed's own preferred measure of labor-market tightness has effectively closed. Second, the quits rate, a proxy for worker bargaining power and a leading indicator for average hourly earnings, is now running below its pre-pandemic baseline. Third, hires have fallen faster than separations, meaning the still-low unemployment rate is being sustained less by robust hiring and more by the absence of layoffs — a fragile equilibrium that historically breaks abruptly rather than gradually.

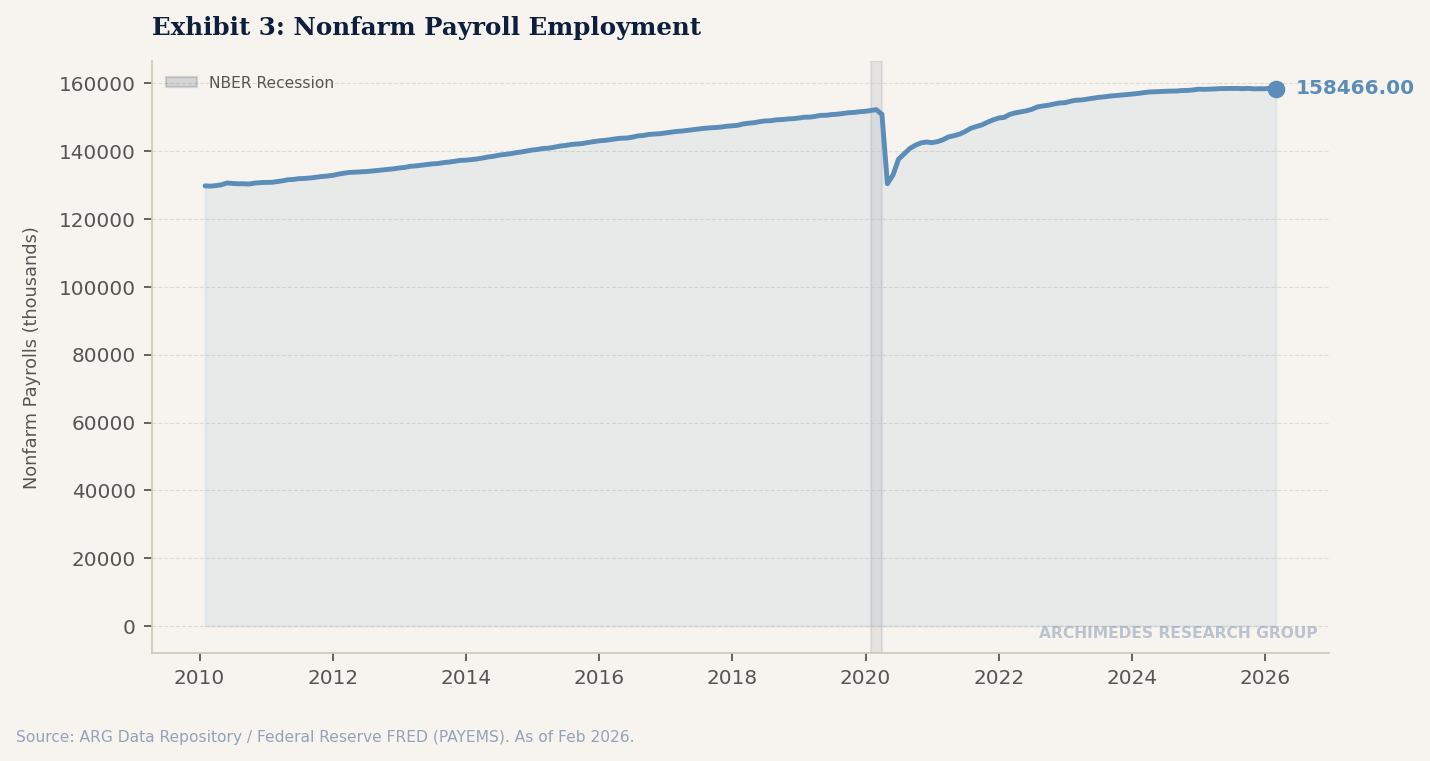

The divergence with the establishment survey is the key tell. Nonfarm payrolls continue to print in the 150–200k range, but birth-death adjustments, part-time substitution, and multiple-jobholder growth explain a disproportionate share of the headline. When JOLTS flows and payroll counts diverge, JOLTS has historically been the earlier and more accurate signal of turning points — notably in late 2000, mid-2007, and early 2020.

Why It Matters Now

The macro context amplifies the signal. Consumer credit data show revolving balances still expanding at a mid-single-digit pace while delinquency rates on credit cards and auto loans have pushed back toward 2010-era highs. A labor market where quits are falling and hiring is slowing removes the primary escape valve households have relied on to outrun rising debt service: the ability to job-switch into higher pay. Strip that away, and the consumer resilience narrative that has underpinned equity multiples since mid-2024 begins to look conditional rather than structural.

Layered on top, the tariff re-escalation announced in March has begun to show up in corporate guidance. Early Q1 earnings commentary from freight, staffing, and regional banks points to cautious hiring plans, rising provision expense, and softer small-business loan demand. These are precisely the sectors where the JOLTS signal is most reliable as a leading indicator — and where the transmission to GDP is fastest.

Implications

For policy: The Fed's reaction function has been explicitly anchored to labor-market balance. With the vacancy-to-unemployed ratio now at neutral and quits below trend, the asymmetry of risks has shifted. A July cut, currently priced at roughly 45%, is likely under-priced; a September cut is near certain absent a re-acceleration in core services inflation.

For credit: Expect spread widening in consumer ABS and high-yield retail as the quits channel closes.

For equities: Consumer discretionary and staffing names carry the highest downside asymmetry; defensive large-cap and rate-sensitive sectors (utilities, REITs, long-duration tech) should outperform on a relative basis into the first cut.

For FDI and capital flows: A softer U.S. labor market, combined with a weaker dollar path, modestly improves the relative attractiveness of U.S. greenfield manufacturing — though tariff uncertainty remains the dominant variable.

Watch List

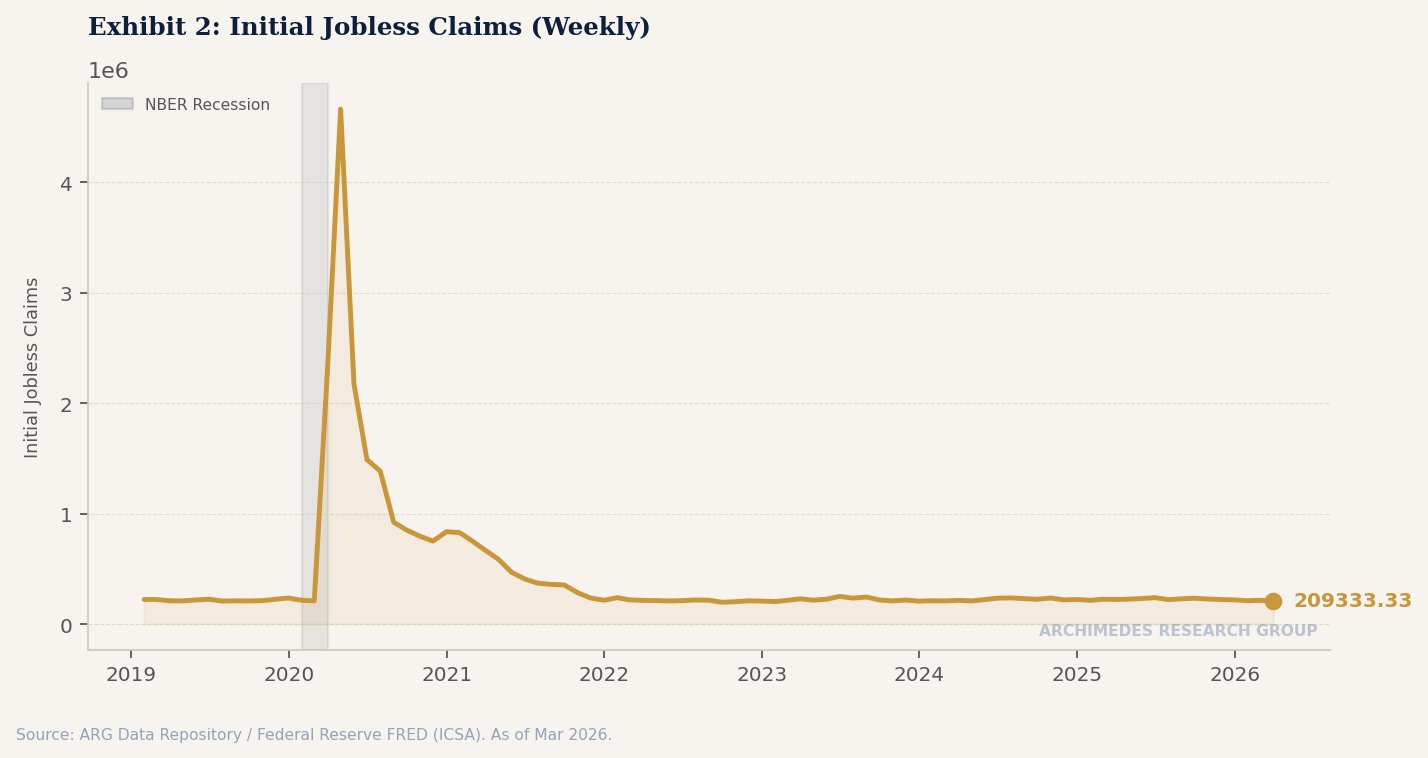

Next JOLTS print (early May) — watch the quits rate and hires; a sub-1.9% quits reading would confirm the fracture. April nonfarm payrolls revisions — prior-month downward revisions have averaged ~40k over the last six releases and are themselves a late-cycle signature. Weekly continuing claims — the most timely cross-check; a sustained move above 1.95 million would corroborate JOLTS. Q1 earnings from staffing bellwethers (ManpowerGroup, Robert Half) and regional banks — guidance here typically leads the BLS data by one to two months. Finally, the May FOMC statement language on "labor market balance" — a shift from "roughly in balance" to any acknowledgment of softening would be the clearest signal that the Fed has internalized the JOLTS message.

Archimedes Research Group. This note reflects analysis of publicly available economic data and should not be construed as investment advice. Distinctions between fact, inference, and forecast are made explicitly in the text above.