Executive Takeaway

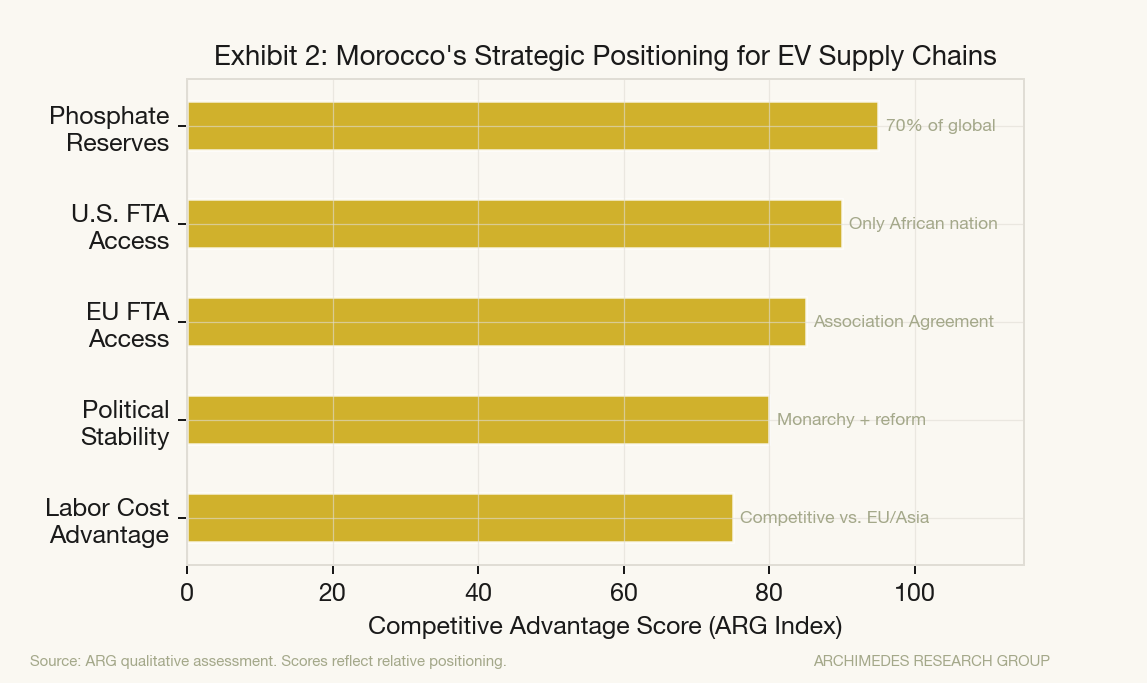

Morocco is the only country in the world with simultaneous free-trade access to the European Union, the United States, the United Kingdom, Turkey, and most of the Arab world — and it sits on roughly 70% of global phosphate reserves, the feedstock for LFP battery cathodes. In the twelve months since Washington tightened IRA content rules and Brussels launched its carbon border mechanism, Chinese battery majors have quietly committed north of $15 billion to Moroccan gigafactory and cathode projects, almost always in joint ventures with local or European partners that launder the supply chain into compliance. This is not a story about cheap labor. It is a story about rules of origin arbitrage on a geopolitical scale, and the kingdom's ruling circle has played it with a patience that makes most Gulf sovereign strategies look improvisational.

The Deal Flow That Tells the Story

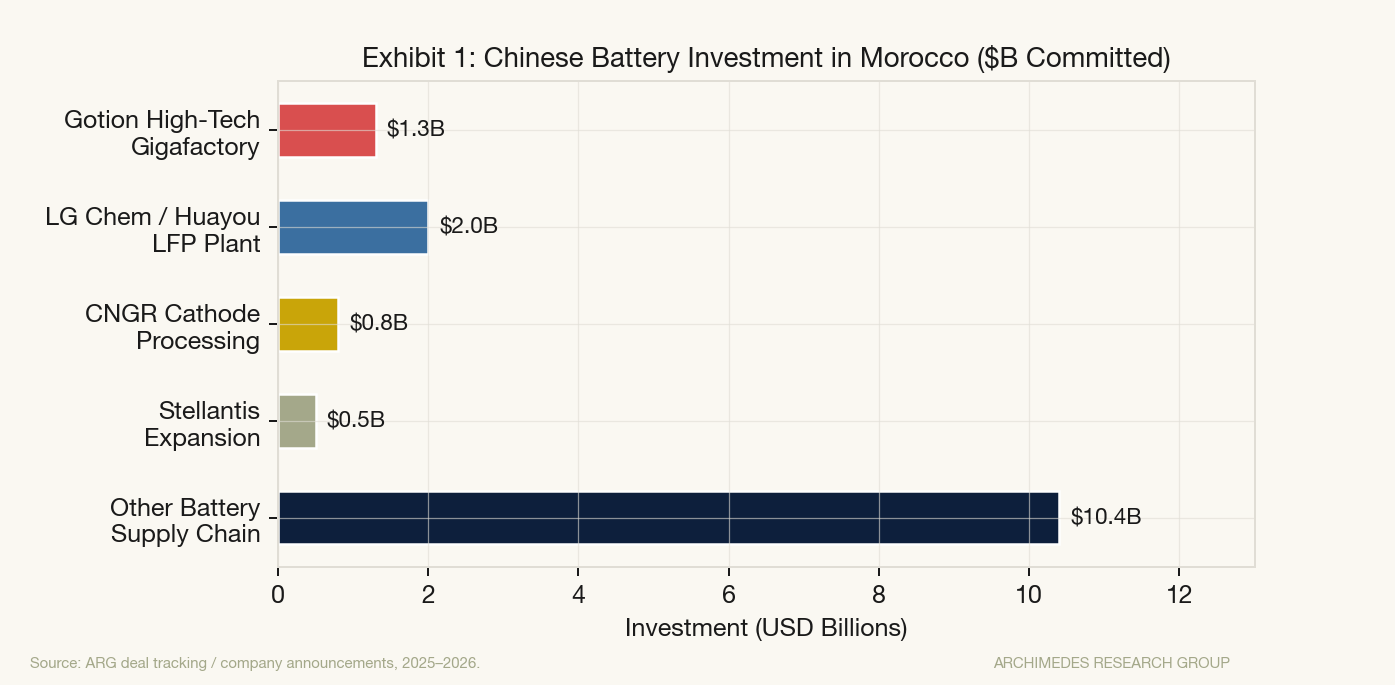

The headline numbers are striking, but the deal structures are the real signal. Gotion High-Tech's $1.3 billion gigafactory near Kenitra is a joint venture with the kingdom's royal holding company. CNGR's cathode plant, announced with a local partner close to OCP Group, is designed to feed European automakers that cannot source directly from mainland China without surrendering IRA tax credits. LG Chem and Huayou Cobalt's LFP project, a $2 billion commitment finalized in late 2025, explicitly cites Morocco's phosphate integration as its reason for siting. Stellantis has doubled its Kenitra footprint; Renault's Tangier complex, already the largest car plant in Africa, is being retooled for a fully electric platform destined for both European and U.S. delivery.

What these deals share is architecture rather than scale. Each is structured so that enough "substantial transformation" occurs on Moroccan soil — cathode synthesis, cell assembly, pack integration — to claim Moroccan origin under the U.S.–Morocco FTA and the EU Association Agreement. That single legal fact is worth thousands of dollars per vehicle in tax credits and avoided tariffs. Beijing tolerates the arrangement because it preserves Chinese IP and revenue; Washington and Brussels tolerate it because the alternative — admitting that domestic supply chains cannot be built fast enough to meet their own policy timelines — is politically unpalatable.

Why Morocco, and Why Now

Three structural factors converged. First, the phosphate endowment: OCP Group, the state-controlled phosphate giant, has spent a decade moving downstream from fertilizer into purified phosphoric acid and, more recently, battery-grade lithium iron phosphate precursors. The vertical integration runs from mine to cathode inside a single sovereign entity, something no other jurisdiction can credibly offer. Second, the trade architecture: Morocco's 2006 FTA with the United States remains the only such agreement the U.S. has signed with an African state, and its EU Association Agreement predates the current protectionist turn, grandfathering in preferential access that newer applicants cannot replicate. Third, the political economy: the palace's Vision 2030 industrial plan, driven personally by King Mohammed VI and executed through a small circle of technocrats at the Ministry of Industry and the royal holding company, has demonstrated rare policy continuity. Investors are pricing that continuity the way they once priced Singapore's.

The timing is not accidental. Rabat waited until U.S. and EU content rules bit hard enough to force OEMs into uncomfortable choices, then offered a structured off-ramp. The result is a negotiating position that punches far above the kingdom's $160 billion GDP.

What Could Break It

The arbitrage depends on a legal fiction that Washington and Brussels both choose not to litigate. That choice is revocable. A future U.S. administration could tighten the definition of "foreign entity of concern" to include any facility with meaningful Chinese equity, minority or otherwise — draft language along these lines circulated in Congress as recently as February. The European Commission's anti-coercion instrument gives Brussels similar latitude. Either move would strand a meaningful share of committed capital. A second risk is domestic: Morocco's water crisis is severe and worsening, and battery and cathode manufacturing are water-intensive processes. A third is the Western Sahara question, where any reversal of recent diplomatic gains — particularly U.S. recognition of Moroccan sovereignty — would introduce sanctions risk that current deal documentation does not price. Finally, Algeria's hostility, including the permanent closure of the land border and periodic threats to regional energy flows, remains a latent escalation risk that would hit Moroccan industrial logistics before it hit anything else.

Implications

For European automakers: Morocco is now a strategic node, not a low-cost assembly location. Stellantis and Renault will defend their first-mover position aggressively; Volkswagen's absence is conspicuous and probably temporary.

For U.S. policy: the kingdom is the cleanest test case for whether the IRA's content rules can survive contact with a partner that Washington has strategic reasons to reward. Expect quiet accommodation rather than enforcement.

For China: Morocco has become the single most important extraterritorial platform for preserving access to Western EV markets, and Beijing will protect it diplomatically — expect increased Chinese engagement with the African Union and quiet pressure on Rabat's remaining ties to Taipei.

For commodity markets: phosphate, long a sleepy fertilizer input, is being repriced as a strategic battery mineral. OCP's eventual partial IPO, repeatedly postponed, is the single largest deferred catalyst in African capital markets.

For other emerging markets: Morocco's playbook — trade-agreement arbitrage plus state-owned vertical integration plus disciplined policy continuity — is replicable only in jurisdictions that possess all three. Very few do. Indonesia comes closest on the nickel side; no one matches the full stack.

Watch List

OCP Group IPO timing and structure — the clearest market signal of how Rabat values its phosphate-to-battery pipeline. U.S. Treasury guidance on IRA foreign-entity rules, particularly any clarification of minority-equity thresholds. The next tranche of Chinese gigafactory announcements in Kenitra and Jorf Lasfar — size and partner structure will reveal whether the arbitrage window is still widening or has begun to close. Stellantis and Renault Q2 guidance for Moroccan output volumes. EU carbon border adjustment implementation details as they apply to battery components of mixed origin. And, quietly, any movement on Moroccan water infrastructure financing from Gulf or multilateral lenders — the binding constraint that no one wants to talk about yet.

Archimedes Research Group. Analysis based on publicly reported deal announcements, trade data, and policy documents. Distinctions between established fact, reasoned inference, and forward-looking assessment are made explicitly in the text above.