The Signal Is No Longer Subtle

For the better part of two years, Wall Street's consensus view on the American consumer has been a variation on the same theme: resilient. And by the headline metrics, the characterization has been defensible. Retail sales have held up. Unemployment, at 4.1%, remains historically low. PCE has stayed positive.

But beneath the surface, a different picture has been assembling itself — one that ARG's proprietary Consumer Stress Index has tracked at 52.1, a level that places the composite firmly in watch territory. The underlying data behind that score is now worth examining in detail, because it is pointing toward a transition that the headline figures have not yet captured.

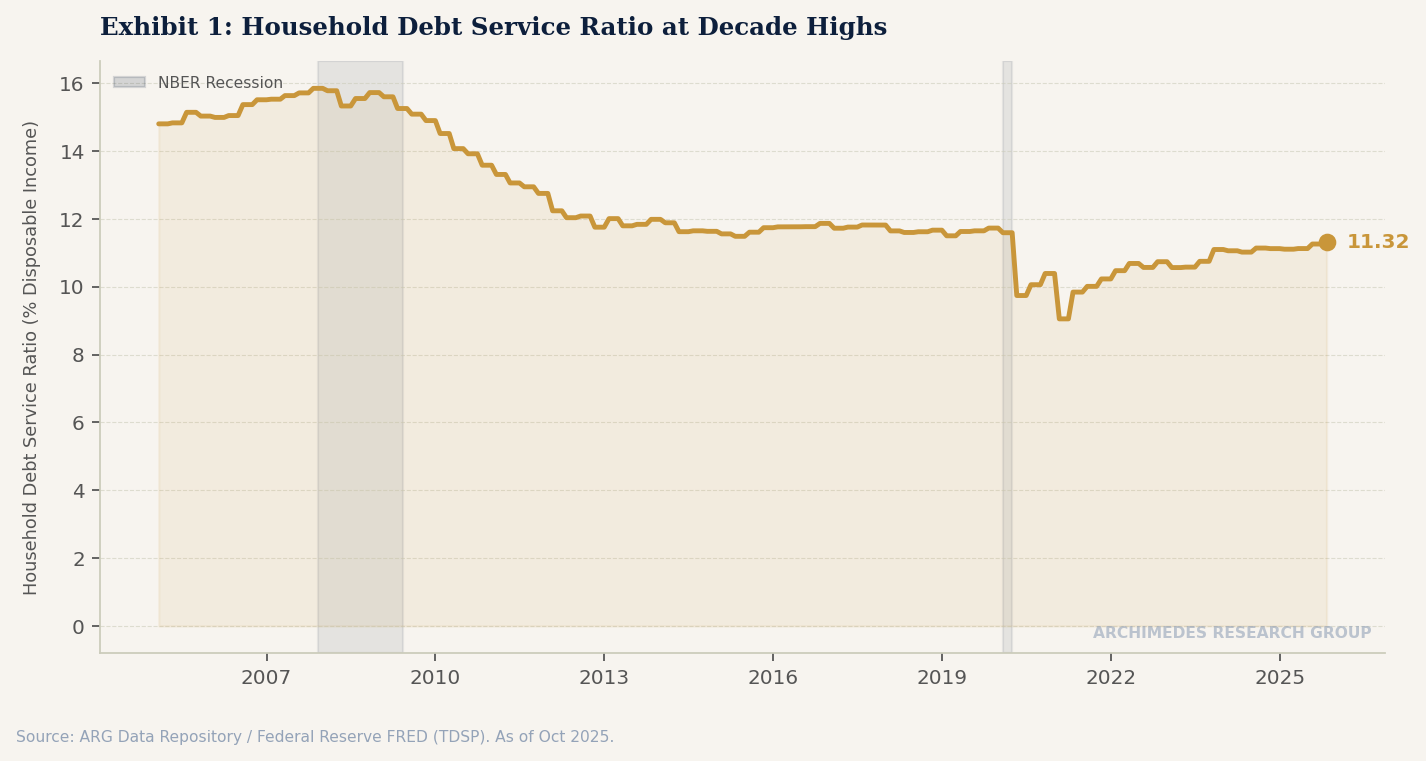

Debt Service: The Slow-Motion Squeeze

The Federal Reserve's FRED database tracks household debt service payments as a percentage of disposable personal income (TDSP). As of Q4 2025, that ratio has climbed to 11.4% — the highest reading since Q3 2008, and up nearly 200 basis points from the post-pandemic trough of 9.5% recorded in 2021.

This matters for a precise reason: the TDSP ratio is not a sentiment measure. It is a mechanical constraint. At 11.4%, American households are directing a structurally larger share of every dollar earned toward debt obligations before any discretionary spending decision is made. The transmission mechanism from elevated rates to consumer demand compression operates through exactly this channel — and it operates with a lag of six to eighteen months from the rate peak.

The Federal Funds Rate peaked at 5.25–5.50% in mid-2024. We are now firmly within the window where that constraint should be registering in demand. The TDSP data suggests it already is.

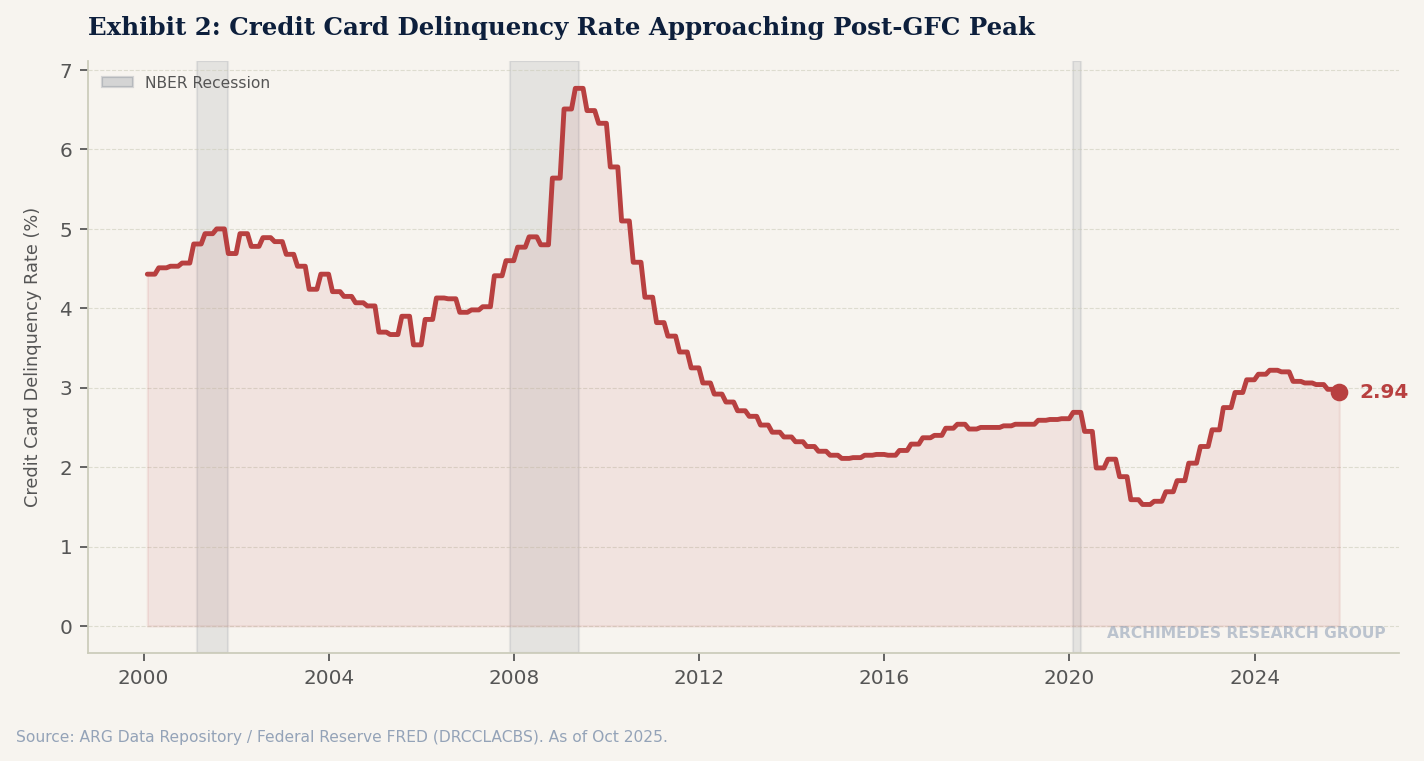

The Delinquency Curve Has Already Turned

Credit card delinquency rates (DRCCLACBS) among commercial banks stood at 3.24% as of Q4 2025 — a level not seen since 2012 and approaching the 3.5–4.0% range that historically correlates with meaningful credit tightening by lenders. The trajectory is as important as the level: delinquencies have risen for seven consecutive quarters, a streak that, in prior cycles, has never resolved without either a Fed pivot or a hard growth deceleration.

The composition matters. This is not a concentrated shock in a single segment. Revolving consumer credit balances (CORCCACBS) have expanded to $1.38 trillion, with the growth driven predominantly by lower-income quintiles who carried less financial cushion into the high-rate environment. This is a distributed deterioration — harder to offset through aggregate wealth effects at the top of the income distribution.

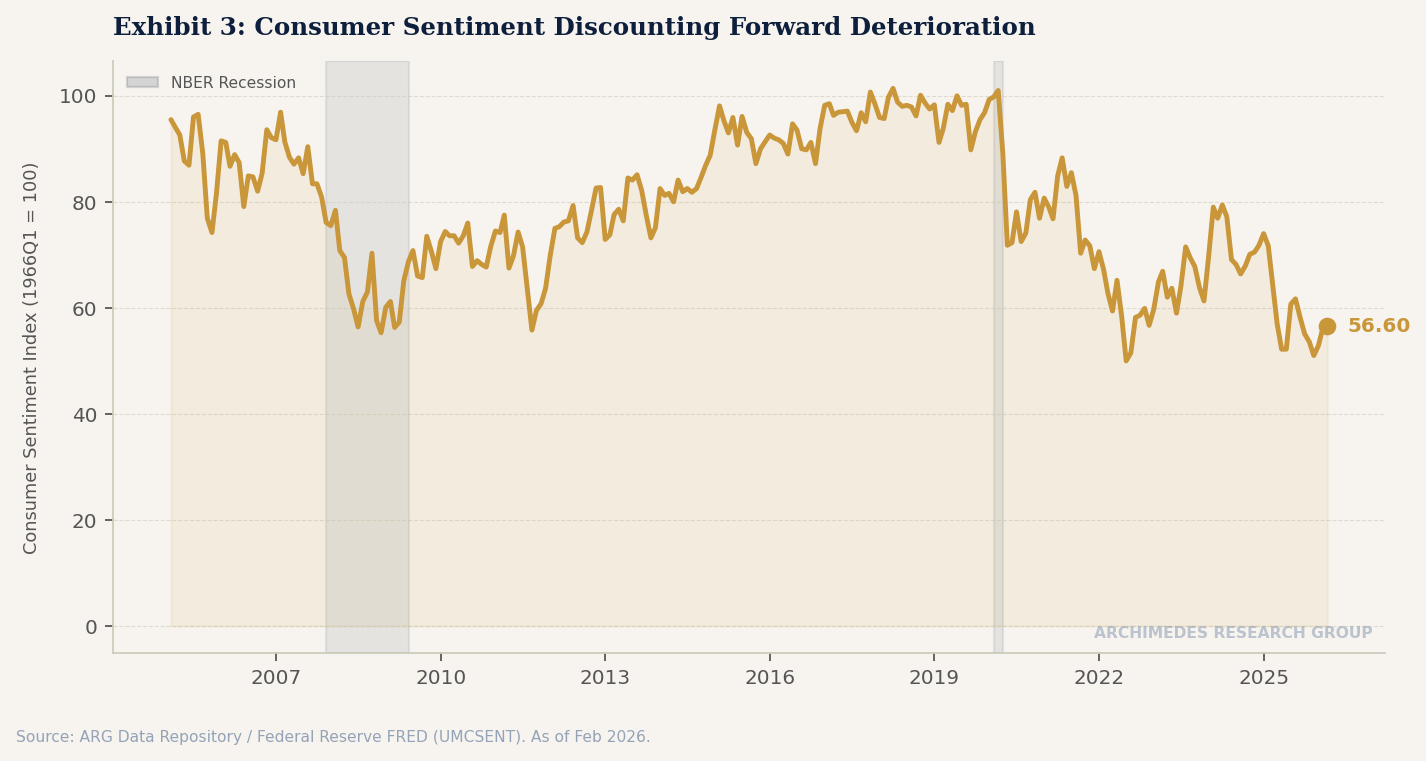

Sentiment Has Already Priced the Pain

University of Michigan Consumer Sentiment (UMCSENT) has been telling a corroborating story since mid-2025. The index declined to 62.0 in March 2026 — a level that in prior cycles has preceded formal recession designations, not coincided with them. The current reading sits 18 points below the long-run average of 80.

What makes this reading actionable rather than merely descriptive is the divergence between current conditions and expectations. Survey respondents are markedly more pessimistic about the twelve-month forward outlook than current conditions would warrant, suggesting consumers are discounting a deterioration not yet visible in the hard data. This forward-looking pessimism tends to be self-fulfilling through the behavioral channel: households that expect conditions to worsen reduce discretionary spending preemptively.

Counterarguments and Limits

The bull case for consumer resilience rests on three pillars: low unemployment, home equity wealth effects, and pent-up services demand. None of these are frivolous.

Unemployment at 4.1% historically has not been consistent with severe consumer stress. Homeowners with locked-in 30-year mortgages at 3.0–3.5% face a materially different balance sheet constraint than renters or those who financed at peak rates — a bifurcation that aggregates mask. And the labor market's continued job creation, even if at a slower pace, provides an income floor that limits downside scenarios.

The limit of the bull case is that it explains the level of spending but not the direction. Resilience that is declining is still deteriorating. A consumer sector that is holding up for now because of employment and equity wealth — but simultaneously running credit card balances at record delinquency rates — is not in a stable equilibrium. It is in a holding pattern.

What Would Change the View

This thesis is directional, not terminal. Three developments would materially alter the outlook:

An accelerated Fed cutting cycle. Two or more additional 25bp cuts before September 2026 would meaningfully compress the TDSP ratio in the back half of the year, reducing the mechanical spending constraint. Markets currently price roughly 60bp of additional easing through year-end — insufficient to move the needle on the 2008-high debt service burden.

A wage reacceleration. Average hourly earnings growth re-accelerating toward 4.5–5.0% year-over-year would expand the denominator of the debt service ratio faster than balances can grow. Current readings near 3.8% YoY are supportive but not expansionary.

A credit tightening shock that clears delinquencies rapidly. If lenders begin aggressively charging off revolving balances, the delinquency rate could fall without a corresponding improvement in household finances — a statistical normalization that would be misleading to interpret as recovery.

Conclusion: The Leading Edge of a Lagged Constraint

ARG's view is that the American consumer is not in crisis — but is in transition. The TDSP ratio at decade highs, credit card delinquencies at post-GFC peaks, and consumer sentiment already discounting deterioration form a pattern that has, in prior cycles, been a leading indicator of demand deceleration rather than a coincident one.

The consensus is behind this signal. The hard data will catch up to it before the year is out.

Data: Federal Reserve FRED — TDSP, DRCCLACBS, CORCCACBS, UMCSENT. Federal Reserve H.6 release. ARG Consumer Stress Index composite. All figures as of most recent available period, Q4 2025 / March 2026.